Pay Dirt

'In 2013, plans for new cities and new districts were sufficient to house about 3.4 billion people, more than twice China’s total population.'

IN SHENZHEN, a short train-ticket and a scrum and a hubbub of people away from Hong Kong, sometime around 2004, a property salesman gave me a pitch – and not the kind of pitch you got every day back then in China.

I was on assignment, fishing for a story rather than an apartment with a view, and the salesman clocked I wasn’t counting bedrooms, his pitches dwindling in enthusiasm until, over stale coffee, I could tell, his spiel was about to shift gears. He became reflective, his eyes narrowed in the direction of the murky city skyline.

I was tempted to ask, “Is there anything uglier than Shenzhen between seasons?” but I shut up.

Zhang – I can’t recall his surname after all the years – steepled his brow with his knuckles, leaned earnestly in my direction and said.

“All this, the apartments, it’s all nothing—none of it,” as if the long morning stroll, the elevator rides, the rummaging in pockets for keys, the prices per square meter and pauses-for views on the run, all of it hustling into a blur, were just a prelude to an announcement

… A big announcement like, “I found Jesus on Sunday and he took me by the hand and I don’t think he’s ever going to leave my side …”

Or worse, “There’s a couple of friends of mine and a CCP membership card waiting for you in the lobby.”

But it wasn’t anything like that.

No, he said:

”The real point,” lingering pointedly on his words, “is that we have to exterminate the Japanese.”

He nodded on the word “exterminate,” as if to pinion in place any doubts I might be secretly harboring.

The conversation froze as I realized he meant it.

It froze again when I replied, “If you’re going to take on Japan, I wouldn’t advise anyone to invest here.”

“The Japanese need to be put in their place,” he said with slightly less zeal than before but still clearly willing to be challenged.

“I don’t think it’s a good idea,” I said, “especially if you’re selling real estate. We’d be close to the front line here.”

We slouched in our chairs and stubbed out our cigarettes.

I smoked back then. Everyone did.

That exchange lingered with me across two decades of watching China’s property machine do what it did—which was everything, and then some, and then too much. Zhang wasn’t selling apartments. He was selling a last-pitch on personal profits and national redemption if the profits weren’t on the next roll.

The property boom was never purely economics. It was the century of humiliation answered in concrete and steel and rising land values. It was China’s declaration that this time—unlike the 1930s, unlike the treaty ports, unlike every humbling encounter with a world secondary to the middle kingdom—was different.

If Zhang was to be believed, the hubris Japan suffered in the mid 19th century was just the beginning. China intended to mete out more of it–hubris with no ending.

Dinny McMahon

Houghton Mifflin Harcourt (March 13, 2018)

288 pages

I reviewed Dinny McMahon’s China’s Great Wall of Debt when it came out in 2018, some four years after my encounter with Zhang, the Shenzhen salesman. Reading it again now, much of it has aged with unusual grace. The first is McMahon’s insistence that China was inflating not a housing bubble but a land bubble.

After all, Chinese buildings crumble to near-non-utility within 2-1/2 decades, leaving the dirt they were built on the only thing worth owning.

That in itself is a complex issue, but one of the things that made McMahon’s China’s Great Wall of Debt so prescient was its insistence that what China was doomed to fall victim to a land bubble, not a housing bubble. Since Chinese buildings depreciate to near-zero over roughly 20 years, it’s the land at their feet that is their value—exactly why the crisis of the 2020s played out through developer and local-government land debt.

It’s all simply state dirt. As McMahon wrote in 2018.

All land in China is owned by some state organ, and technically none of it is for sale. However, in 1988, the Party changed the constitution so that the right to use the land (but not to own it) could be bought and sold under long-term leases. Today, developers get to lease land zoned for residential use from the state for seventy years, and commercial land for fifty years. (Generally speaking, no one expects land to revert to the government at the end of a lease, and for simplicity’s sake I refer to “leases” as “sales” throughout this book.) At its heart, this system allows China’s Communists to hold on to the traditional principle that all land is collectively owned by the people. But the constitutional change was a clever compromise that allowed the government to turn land into cash when, less than a decade into the reform period that followed the ascent of Deng Xiaoping as supreme leader, the Party found that it didn’t have the funds it needed to march the economy into modernity.

It’s precisely why the reckoning of the 2020s arrived not as a wave of defaulting homeowners, American-style, but as a pile-up of insolvent developers and local governments—developers such as Evergrande and Country Garden and a legion of financing vehicles—all of whom had bet the farm, quite literally, on the dirt the chickens scrabbled and hooted in–being organic and free-range and all.

But McMahon also brought the lights to bear on China’s shadow-banking arithmetic. The credit from the shadow-banking system, he reckoned, roughly doubled to some 80% of GDP in the middle of 2016, from about 40% in 2014. That number turned out to be less a curiosity than a countdown, ticking down to Beijing’s 2020-to-2021 “three red lines” policy … The curtains are still drawing on the red lines.

When McMahon was researching his book—still writing it—its direst predictions lay in an unrealized future—unrealized but close. Within two years, Beijing was implementing its so-called “three red lines.”

Their aim was to stop the endless borrowing and building on investments that would be unlikely to outlive their down-payments.

The “three red lines”—a CCP swift move on its own Marxism-with-Chinese-characteristics governance system–was based on how much debt property developers could carry, based on three leverage ratios: debt-to-cash, debt-to-equity, and debt-to-assets. Developers were sorted into categories depending on how many of the three lines they breached, and that determined how much new debt they were allowed to take on going forward — those breaching more lines faced tighter restrictions on further borrowing.

It was a deliberately designed policy: Beijing had decided the sector had become too large and too dangerous—real estate had reached roughly a quarter of the economy—and chose to force developers to deleverage rather than let the bubble keep inflating. The predictable result was a wave of defaults across the industry (Evergrande in 2021, Country Garden in 2023, and dozens of others).

Evergrande–not China’s biggest steamroller–but definitely a name everyone knew crossed all three lines, resulting in a liquidity crisis and its later insolvency.

In light of everything that has happened since—Evergrande’s shock collapse, the near-implosion of Country Garden, once the industry’s biggest developer by sales, and a local-government financing-vehicle crisis still working its way through the system like a kidney stone—McMahon’s treatise is less a warning than an advance autopsy.

McMahon’s 2018 argument was structural. China’s debt-driven growth model was not a policy choice that could be reversed by a sufficiently determined leadership. It was a system with its own internal logic, its own incentive architecture, its own immune responses to reform.

Local governments responsible for 80% of expenditures but receiving only half of tax revenues had filled the gap by monetizing land—turning the one asset the state controlled absolutely into the fuel that ran everything else: infrastructure, ghost cities, new districts built to house populations that didn’t exist and in which some cases never arrived—all of it funded by land sales, underwritten by a banking system staffed by officials whose political careers depended on growth figures they had every incentive to inflate and no incentive to question.

The numbers McMahon assembled raised eyebrows then.

They look conservative now. Between 2007 and 2015, China was responsible for 63% of all new money created globally. In 2013, plans for new cities and districts were sufficient to house 3.4 billion people—more than twice China’s total population. The average newly constructed building had a lifespan of twenty years. Developers were paying more for land than the apartments they planned to build on it could ever recover. The Bank of China’s own chairman described wealth management products as a Ponzi scheme and then, in the same column, defended their utility.

What McMahon captured when I reviewed the book in 2018, was a system that knew it was broken and kept building anyway. It was as if he had got hold of the operating instructions of a system that had institutionalized its own dysfunction.

On the fringes, the operating systems built ghost cities in Inner Mongolia, the Chinese property investment companies ventured into Johor, where they built what is known as Malaysia’s China-built ghost city, Forest City. It left the seaside enclave of Sihanoukville a launching pad for a scamming vehicle that brought Cambodia to near full-on war with Thailand. It went into the condo markets of Bangkok and Ho Chi Minh City and the landed property markets of Sydney and Melbourne.

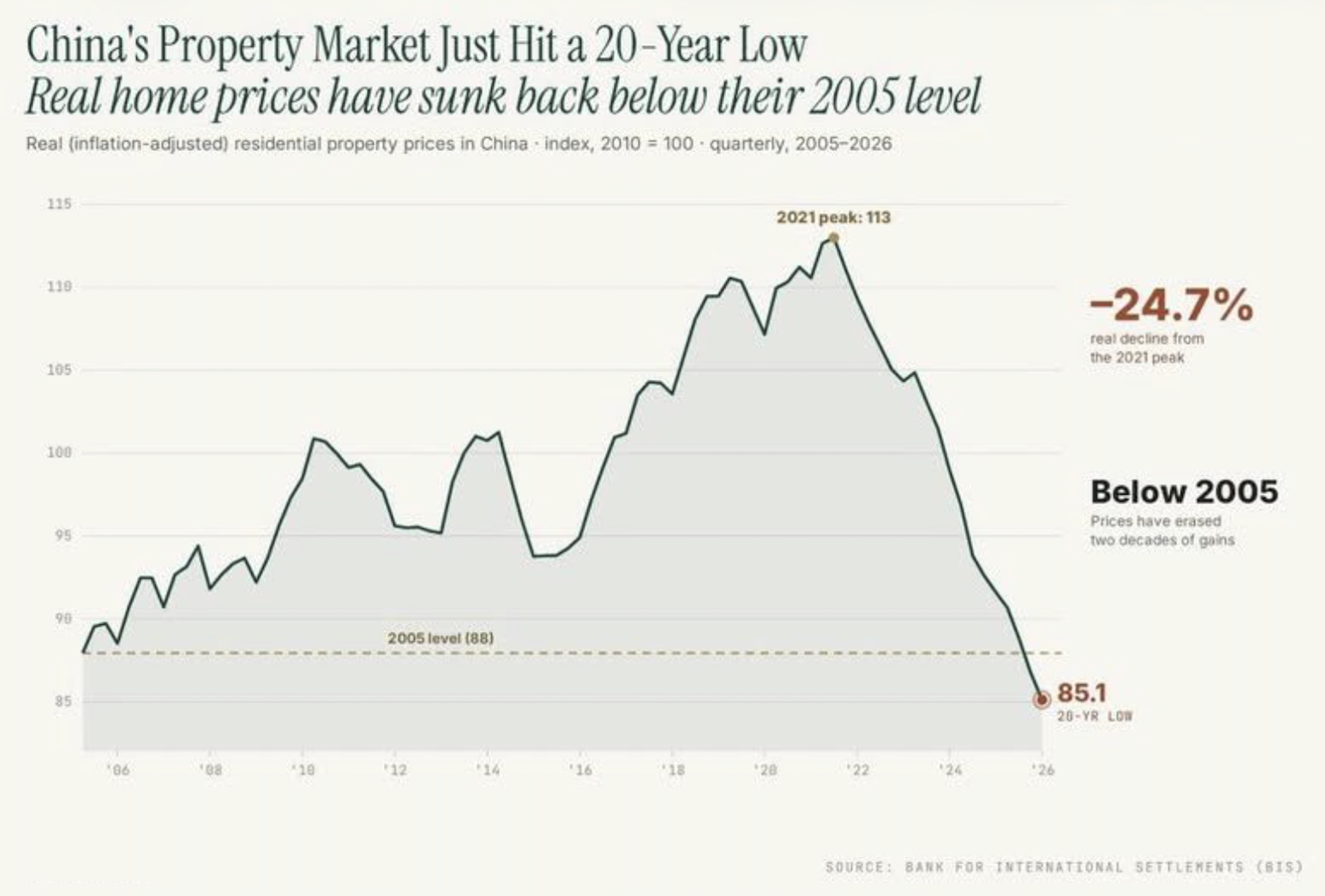

Shenzhen itself—the city where Zhang, my real estate guy of times past, made his pitch—has since watched its own apartments do exactly what he never mentioned: existing home prices there have fallen by close to half from their 2020 peak.

Zhang was on the money more than he knew.

China awakened Japan.

As for property, a condo with a view in Shenzhen or a small renovated former onsen hotel an hour out of Tokyo? Both come with problems, but sensibly one would invest in Japan and not be arrested for holding literary events.

A version of this review first appeared in the author’s personal website, christaylorink.